Digital banks are a new type of financial institution that provides banking services exclusively through digital channels. They do not have any physical branches, and all of their transactions are conducted online or through mobile apps. Bangladesh is going to initiate digital banks in the country as a step in the Smart Bangladesh Journey.

Table of Contents

Digital Banks in Bangladesh

So far, there are no digital banks operating in Bangladesh. However, there are a number of companies that are planning to set up digital banks in the country including banks, mobile financial services (MFS) providers, insurance companies, fintechs, and many more. There were 52 applications for digital banks.

On October 22, 2023, Bangladesh Bank declared its stance on the approval of digital banks issuing Policy Approval to eight entities. The decision was taken at a board meeting held at the Bangladesh Bank headquarters, with Governor Abdur Rouf Talukder in the chair. Among them, 2 entities (Nagad Digital Bank PLC and Kori Digital PLC of ACI) were awarded Letters of Intent (LOI) to complete formalities in 6 months, 3 bank-led entities (DG10 Bank Plc by 10 banks, bKash Digital Bank PLC by BRAC Bank, DigitALL Bank by Bank Asia) will open digital wings in 3 months, 3 fintech entities (Smart Digital Bank, North East Digital Bank, Japan-Bangla Digital Bank) to get Letters of Intent (LOI) after successful start of operation of the first banks.

According to one circular signed by the Bangladesh Bank’s Deputy Governor Nurun Nahar, “Nagad Digital Bank PLC” was listed as a scheduled bank on 3 June 2024 making it the first scheduled digital bank in Bangladesh. However, the approval has been on pause for reasonable grounds and Bangladesh Bank invited applications again from interested for establishing digital banks on 21 August 2025.

Mohammad Shahriar Siddiqui, Director (BRPD) of Bangladesh Bank hands over a copy of the digital bank licence to Tanvir A Mishuk, founder and chief executive officer (CEO) of Nagad Ltd.

The central bank on June 21 invited applications for establishing digital banks and set the deadline for applications on August 1. To facilitate proper documentation in the application process, the deadline has been extended to August 17, 2023, keeping all the previous conditions in place. After August 17, BB reviewed the applications and related documents to issue a no-objection certificate for the proposed digital banks in 3 committees.

Then, BB decides based on a 100-mark scoring on 3 factors namely

(1) Business aspect,

(2) The context of a business, and

(3) Understanding the market segment, technology, and security.

9 Entities securing above 60 marks were considered for approval. One application was insurance-led and the board scrapped that. So, 8 entities are positively considered for approval.

So, Nagad Digital Bank PLC and Kori Digital PLC of ACI) are awarded Letters of Intent (LOI) to complete formalities in 6 months, 3 bank-led entities to open digital wings as they have licenses, 3 fintech entities to get LOI after operations of the first 2 Digital Banks.

Digital banks have the potential to bring financial services to a wider range of people in Bangladesh. They can also help to reduce the cost of banking and make banking more convenient and accessible.

Digital Bank Defined

A digital bank is a type of financial institution that operates primarily online, offering banking services and products through digital channels such as websites and mobile applications. It functions without physical branch locations, allowing customers to access and manage their accounts conveniently from their devices.

Digital banks leverage technology to provide a range of banking services, including opening and managing accounts, conducting transactions, transferring funds, making payments, and accessing financial information. They often prioritize user-friendly interfaces, seamless digital experiences, and enhanced security measures to provide a convenient and efficient banking experience for customers. Customers can open accounts, deposit money, transfer funds, pay bills, and access other banking services through the bank’s website or mobile app.

At what stage does the digital bank make a profit?

The timeline for a digital bank to become profitable is a complex matter that depends on various factors, including the bank’s business strategy, level of investment, and market conditions. Here are some key points to consider regarding when a digital bank might reach profitability:

1. Business Strategy: The digital bank’s business strategy plays a critical role in determining when it can become profitable. Some digital banks may choose to take a conservative approach, focusing on gradual customer acquisition and steady growth. Others might adopt a more aggressive strategy, aiming to capture a larger market share in a shorter timeframe. The chosen approach will influence the timeline for profitability.

2. Initial Investment: The amount of investment made in the digital bank is a significant factor. As mentioned, the minimum paid-up capital required for a digital bank is Tk125 crore, but some may invest more, such as Tk200 crore. Banks with greater financial resources can scale their operations more quickly, invest in advanced technology, and allocate substantial funds for marketing and customer acquisition.

3. Technology Investments: Digital banks heavily rely on technology to operate efficiently and provide innovative services. Significant investments in technology are required for developing robust digital platforms, ensuring cybersecurity, and offering a seamless user experience. The level of technology investment can impact the speed at which a digital bank can reach profitability.

4. Marketing and Customer Acquisition: Digital banks need to invest in marketing and customer acquisition efforts to attract a substantial customer base. The aggressiveness and effectiveness of these marketing campaigns can significantly impact the pace at which customers are acquired, which, in turn, affects the timeline for profitability.

5. Market Conditions: The competitive landscape and market conditions also play a role. If a digital bank faces fierce competition from established banks or other digital banking players, it may take longer to gain market share and become profitable. Conversely, in less competitive markets, profitability may be achieved more quickly.

6. Regulatory Compliance: Compliance with regulatory requirements and guidelines is essential for digital banks. The extent to which a digital bank can swiftly navigate regulatory challenges and meet compliance standards can influence its path to profitability.

Guidelines to Establish Digital Bank

Bangladesh is one of the countries that is in the process of embracing digital banking. The Bangladesh Bank, the central bank of Bangladesh, has approved a framework for the establishment of digital banks in the country on June 15, 2023. The framework requires digital banks to have a minimum capital of Tk125 crore and to offer “efficient, low cost, and innovative” financial products and services. However, Bangladesh Bank updated its stance on 21 August 2025 by increasing the capital to Taka 300 crore from previous 125 crore.

Here are some key points from the guidelines for the establishment of digital banks:

- Digital banks must have a minimum paid-up capital of Tk. 125 crore.

- Digital banks must offer “efficient, low-cost, and innovative” financial products and services.

- Digital banks must have a strong corporate governance framework.

- Digital banks must comply with all applicable laws and regulations.

- Digital banks must submit a business plan to the Bangladesh Bank for approval.

The Bangladesh Bank has also set out a number of requirements for digital banks, including:

- They must have a strong IT infrastructure.

- They must have a robust risk management framework.

- They must have a customer-centric approach.

- They must be committed to financial inclusion.

The guidelines on the establishment of digital banks in Bangladesh are designed to promote the growth of this new and innovative sector. The Bangladesh Bank is confident that digital banks will play a significant role in increasing financial inclusion and economic development in the country.

Here are some additional details:

- Digital banks are allowed to offer a wide range of financial products and services, including savings accounts, current accounts, loans, and investment products.

- Digital banks are not allowed to open physical branches. However, they can offer their services through online channels, mobile apps, and call centers.

- Digital banks are subject to the same regulations as traditional banks, including those related to customer protection, anti-money laundering, and Know Your Customer (KYC).

The Bangladesh Bank has said that it expects to receive applications for the establishment of digital banks in the near future. The first digital banks in Bangladesh are expected to start operating in 2023.

Paid-Up Capital for Branchless Banks

There has been a circular by Bangladesh Bank on June 15, 2023, disclosing that the paid-up capital for and new bank be BDT 500 crores whereas the capital for a branchless bank is BDT 125 crores.

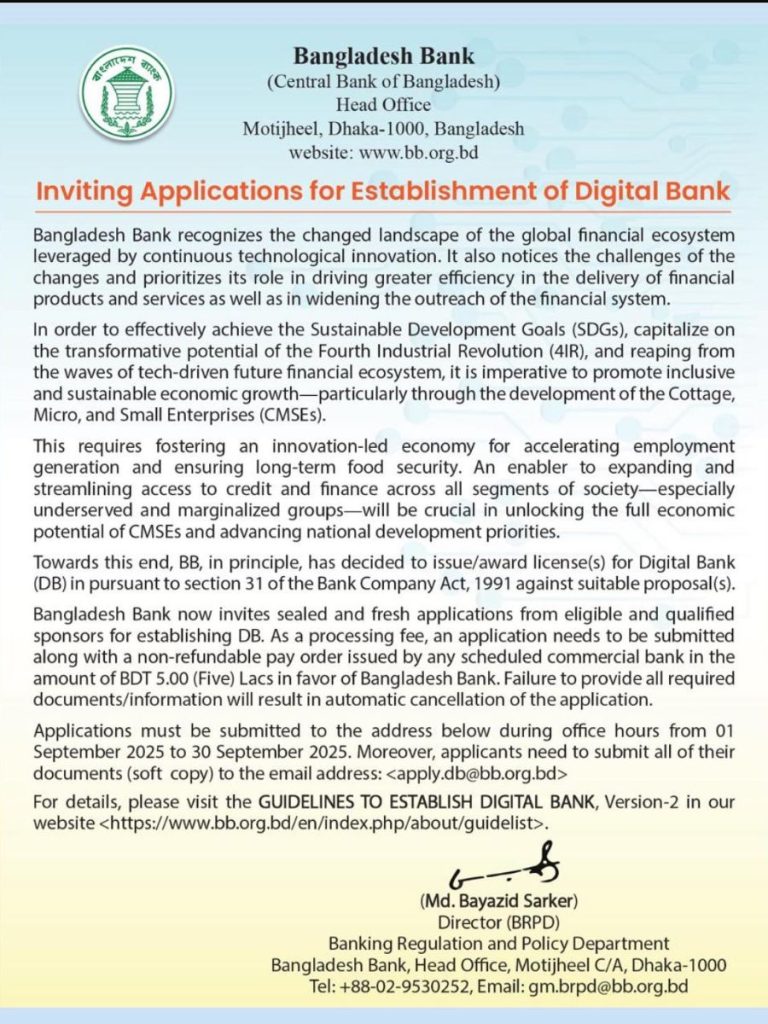

Establishment of Digital Bank

Digital innovation is continuously modifying the landscape of the financial

system all over the world. Bangladesh Bank (BB) promotes an enabling regulatory

environment allowing innovation to make a robust, efficient and secured financial

system. Accordingly, BB recognizes the role of digital platforms and usage of

artificial intelligence in driving greater efficiency in the delivery of financial

products and services and in widening the outreach of the financial system.

Towards this end, BB has decided in principle to issue license for full-fledged

digital banking. Now BB is intending to issue license for Digital Banks (DB) in

pursuant to section 31 of the Bank Company Act, 1991. The terms and conditions

for establishment of DB include (but not limited to):

- Must be a public limited company licensed under section 31 of the Bank

Company Act, 1991; - Initial minimum Paid-up capital BDT 125.00 (One hundred twenty-five)

crores shall be provided by the sponsors; - The minimum shareholding stake of each sponsor shall be BDT 50.00 (Fifty)

Lac; - Sponsors’ contribution to the share capital of the proposed DB will be

required to be out of net worth declared to the Tax authorities. Sponsors’

contribution out of borrowings from bank or financial institutions or from

anywhere else, even from family members, shall not be acceptable; - The sponsors/directors must qualify the Fit and Proper Test (FPT) criteria

applicable for the proposed directors of DB; - Bangladesh Bank now invites applications for establishing DB

through the License Application Portal, web link of the portal is

https://license.bb.org.bd - The amount of BDT 5.00 (Five) Lacs should be paid as a non-refundable

application processing fee through the same web portal; - The License Application Portal will remain open for accepting applications

from 21 June 2023 to 1 August 2023.

For details, please visit the GUIDELINES TO ESTABLISH DIGITAL BANK in Bangladesh Bank website https://www.bb.org.bd/en/index.php/about/guidelist.

To facilitate proper documentation in the application process, the deadline has been extended to August 17, 2023, keeping all the previous conditions in place.

Benefits of digital banks in Bangladesh

When a digital bank will be introduced in Bangladesh, there are several benefits that individuals and businesses can expect. Here are some of the benefits of digital banking in Bangladesh:

- Accessibility: Digital banks provide easy access to financial services, allowing customers to perform transactions and access their accounts anytime, anywhere through digital platforms such as mobile apps and websites. This accessibility eliminates the need to visit physical bank branches, saving time and effort.

- Convenience: With a digital bank, customers can conveniently manage their finances from the comfort of their homes or offices. They can check account balances, transfer funds, pay bills, apply for loans, and perform other banking activities online, without the need to queue or wait for banking hours.

- Cost-Effectiveness: Traditional banks often have various fees and charges associated with their services. Digital banks tend to offer lower fees or even free transactions for certain activities, such as online transfers and bill payments. This cost-effectiveness benefits both individuals and businesses, as they can save money on banking services.

- Financial Inclusion: Digital banking can play a vital role in promoting financial inclusion in Bangladesh. It enables individuals who may not have had access to traditional banking services, such as those in remote areas or with limited mobility, to participate in the formal financial system. Digital banking bridges the gap and provides access to essential financial services to a wider population.

- Enhanced Security: Digital banks prioritize security measures to protect customer information and transactions. They employ advanced encryption technologies, multi-factor authentication, and fraud detection systems to ensure the safety of customer data. This enhanced security instills confidence in customers and mitigates risks associated with traditional banking methods, such as lost or stolen checks or physical cash.

- Streamlined Processes: Digital banking streamlines processes by automating various tasks. For instance, opening an account or applying for a loan can be done digitally, reducing paperwork and processing time. The automation of routine tasks improves efficiency and allows banks to focus on providing better customer service and personalized assistance.

- Innovation and Advanced Features: Digital banks often leverage technological advancements to offer innovative features and services. This can include personalized financial management tools, real-time notifications, automated savings options, and integration with third-party platforms for seamless financial management. These advanced features enhance the overall banking experience for customers.

- Financial Education: Digital banks can provide educational resources and tools to promote financial literacy and empower customers to make informed financial decisions. They can offer interactive tutorials, budgeting tools, and personalized recommendations to help individuals and businesses better understand their financial situation and plan for the future.

- Increased Competition: The introduction of a digital bank in Bangladesh will likely stimulate competition within the banking sector. Traditional banks may need to enhance their digital offerings and improve customer experience to remain competitive. Increased competition often leads to improved services, lower costs, and better products for customers.

- Economic Growth: A digital bank can contribute to the overall economic growth of Bangladesh. By facilitating financial transactions, promoting entrepreneurship, and supporting small and medium-sized enterprises (SMEs), digital banking can drive economic activity, create jobs, and spur innovation in the financial sector.

- Financial Tracking and Analysis: Digital banks offer advanced tools and features that enable users to track and analyze their financial activities in real-time. Through intuitive dashboards and reports, customers can gain insights into their spending patterns, set budgeting goals, and identify areas for potential savings. This financial tracking and analysis empower individuals and businesses to make data-driven financial decisions and improve their overall financial well-being.

- Seamless International Transactions: Digital banks often provide integrated foreign exchange services and seamless international money transfers. This is particularly beneficial for individuals and businesses engaged in cross-border transactions, such as importing, exporting, or sending remittances. By eliminating the need for intermediary banks or currency exchange services, digital banks can offer faster, more cost-effective, and transparent international transactions.

- Personalized Customer Support: Digital banks typically prioritize customer service and support. Through digital channels such as chatbots, live chat, or email, customers can receive prompt assistance for their queries or concerns. Additionally, digital banks often offer personalized recommendations and tailored financial advice based on customers’ transaction history and financial goals. This personalized customer support fosters a stronger customer-bank relationship and enhances the overall banking experience.

- Integration with Fintech Services: Digital banks can integrate with a wide range of financial technology (fintech) services, including payment gateways, digital wallets, investment platforms, and accounting software. This integration allows customers to seamlessly connect their digital bank accounts with other fintech tools they use for their financial activities. For example, individuals can link their digital bank accounts to e-commerce platforms for streamlined payment processing, while businesses can integrate their digital bank accounts with accounting software for automated bookkeeping. This integration simplifies financial management and increases efficiency for customers.

- Green Banking: Digital banks are inherently eco-friendly as they significantly reduce the need for paper-based transactions and physical documentation. By promoting paperless banking, digital banks contribute to environmental sustainability and conservation. The reduction in paper waste, carbon emissions from transportation, and energy consumption associated with physical bank branches positively impacts the environment. Embracing digital banking in Bangladesh can be a step towards creating a more sustainable and greener banking industry.

These benefits collectively illustrate the potential impact and advantages that a digital bank can bring to Bangladesh, empowering individuals, businesses, and the economy as a whole. These benefits further highlight the advantages of having a digital bank in Bangladesh, encompassing aspects such as financial management, international transactions, customer support, integration with fintech services, and environmental sustainability.

The growth of digital banks in Bangladesh is likely to be driven by a number of factors, including:

- The increasing availability of smartphones and internet access in Bangladesh.

- The growing demand for convenient and affordable banking services.

- The regulatory support for digital banking from the Bangladesh Bank.

As digital banking continues to grow in Bangladesh, it is expected to have a positive impact on the country’s economy. It will help to increase financial inclusion, reduce the cost of banking, and make banking more convenient and accessible. It will also help to promote innovation in the banking sector.

Challenges of digital banks in Bangladesh

Here are some of the challenges that digital banks in Bangladesh may face:

- Limited Digital Infrastructure: Bangladesh may face challenges related to limited digital infrastructure, particularly in remote areas. The availability and quality of internet connectivity, access to smartphones or computers, and digital literacy levels could impact the adoption and usage of digital banking services. Efforts to improve digital infrastructure and promote digital literacy would be crucial in overcoming this challenge.

- Low internet penetration: The internet penetration rate in Bangladesh is still relatively low. This means that there are a large number of people who do not have access to the internet, and who therefore cannot use digital banking services. Digital banks need to find ways to reach these people, such as through mobile banking.

- Security: Digital banks need to ensure that their systems are secure from cyberattacks. This is a major challenge, as cyberattacks are becoming increasingly sophisticated. Digital banks need to invest in robust security measures, such as firewalls, intrusion detection systems, and encryption. They also need to educate their employees about cybersecurity risks and how to protect customer data.

- Trust and Security Concerns: Building trust in digital banking is essential for its success. Customers may have concerns regarding the security of their personal and financial information when using digital platforms. Ensuring robust security measures, implementing strong data protection protocols, and transparently communicating security measures to customers are crucial to address these concerns and build trust in digital banking.

- Regulatory Framework: Establishing a regulatory framework that addresses the unique challenges and risks associated with digital banking is vital. The regulatory authorities need to develop guidelines and regulations that protect customers’ interests, ensure fair competition, and prevent fraudulent activities. Striking a balance between innovation and consumer protection would be a key challenge for regulators.

- Customer Education and Adoption: Educating customers about the benefits and functionalities of digital banking can be a challenge. Many individuals may be accustomed to traditional banking methods and may require support and guidance to transition to digital platforms. Digital banks would need to invest in educational campaigns and user-friendly interfaces to encourage customer adoption and address any concerns or resistance.

- Financial Inclusion: While digital banking has the potential to promote financial inclusion, certain segments of the population, such as the elderly, individuals with disabilities, or those in remote areas, may face barriers in accessing and using digital banking services. Ensuring that digital banking services are inclusive and accessible to all individuals, regardless of their age, location, or abilities, would be a challenge that needs to be addressed.

- Cybersecurity Threats: As digital banking relies heavily on technology and online platforms, the risk of cyberattacks and data breaches increases. Cybersecurity threats, such as hacking attempts, phishing attacks, or malware, pose significant challenges to digital banks. Implementing robust cybersecurity measures, regular audits, and staying updated with evolving security threats are crucial to safeguard customer data and maintain trust.

- Cash-Dependent Economy: Bangladesh still has a significant portion of the population that relies heavily on cash transactions. Encouraging a shift from cash to digital payments can be a challenge, as it requires changing deeply ingrained behaviors and addressing concerns related to the reliability and acceptance of digital payment methods across various sectors, including retail, transportation, and informal markets.

- Collaboration with Traditional Banks: Digital banks may face challenges in collaborating and partnering with traditional banks. Establishing interoperability between digital and traditional banking systems, addressing concerns about competition, and fostering collaboration for the benefit of customers and the overall banking ecosystem would require effective communication and cooperation between digital banks and traditional financial institutions.

- Competition from traditional banks: Traditional banks are also offering digital banking services. This means that digital banks face competition from traditional banks, which have a larger customer base and more resources. Digital banks need to find ways to differentiate themselves from traditional banks, and they need to offer products and services that are attractive to customers.

- Regulatory Compliance and Anti-Money Laundering (AML): Digital banks must comply with regulatory requirements and anti-money laundering regulations. Implementing robust Know Your Customer (KYC) procedures, monitoring transactions for suspicious activities, and ensuring compliance with AML regulations pose challenges, particularly as digital banking transactions can be conducted remotely and across borders.

- Scalability and Customer Service: As digital banks grow and attract a larger customer base, ensuring scalability and providing consistent and high-quality customer service can be challenging. Maintaining responsive customer support, resolving customer queries and concerns promptly, and scaling up technological infrastructure to handle increased transaction volumes are essential for a seamless customer experience.

Addressing these challenges will be crucial for the successful implementation and growth of digital banks in Bangladesh. Despite these challenges, the future of digital banking in Bangladesh looks bright. The country has a large population that is increasingly using smartphones and internet access. The Bangladesh Bank is supportive of digital banking, and there is a growing demand for convenient and affordable banking services. As these factors continue to drive growth, digital banking is expected to play an increasingly important role in the Bangladeshi economy.

What is the difference between digital bank account and normal account?

A digital bank account and a normal account differ primarily in their mode of operation and accessibility. Here are the key differences:

- Mode of Operation: A normal account, also known as a traditional bank account, typically requires in-person visits to a physical branch for account opening, transactional activities, and customer service. On the other hand, a digital bank account operates entirely online, allowing customers to open and manage their accounts through web-based platforms or mobile applications.

- Account Opening: Opening a normal bank account usually involves filling out paper forms, providing physical documents such as identification and proof of address, and often requires waiting in queues at the bank. Digital bank accounts, in contrast, can be opened entirely online with a few simple steps. Applicants can submit their information and required documents electronically, eliminating the need for physical paperwork.

- Accessibility: Digital bank accounts provide the convenience of 24/7 accessibility. Customers can access their accounts and perform various banking transactions anytime and anywhere using their smartphones, tablets, or computers with an internet connection. Traditional accounts may have limited banking hours, and accessing account information or conducting transactions often requires visiting a physical branch or using an ATM.

- Cost and Fees: Digital banks often offer lower fees and charges compared to traditional banks. They may have fewer overhead costs associated with physical infrastructure, which allows them to pass on the savings to customers in the form of reduced fees or no fees for certain services. Traditional banks may have higher fees due to their physical branch network and operational expenses.

- Customer Support: Traditional banks typically offer in-person customer support at their branches, along with phone and email assistance. Digital banks usually provide customer support through online channels, such as live chat, email, or dedicated customer service hotlines. Some digital banks may also offer video chat options for more personalized assistance.

- Additional Features: Digital banks often provide innovative features and services beyond basic banking functions. These can include budgeting tools, spending analytics, real-time transaction notifications, integration with third-party financial apps, and faster payment options like peer-to-peer transfers or digital wallets. Traditional banks may also offer some of these features but may be slower to adopt newer technologies.

It’s worth noting that the specific features and offerings of digital and traditional bank accounts can vary between different financial institutions. It’s always a good idea to research and compare the services, fees, and security measures provided by various banks before choosing the one that best suits your needs.

Digital/Online banking vs digital bank

Here’s a table comparing digital banking and a digital bank:

| Criteria | Digital Banking | Digital Bank |

|---|---|---|

| Definition | The use of electronic channels for banking | A bank that operates primarily online |

| Services | Online banking, mobile banking, digital wallets | Full range of banking services offered online |

| Branches | May have physical branches | No physical branches |

| Accessibility | Available to customers of traditional banks | Available to anyone with internet access |

| Account Opening | Usually requires an existing bank account | Can open a new account entirely online |

| Customer Support | Online chat, phone, email support | Online chat, phone, email support |

| Technology | Uses online platforms, mobile apps | Utilizes advanced technology for digital banking |

| Transaction Limits | Subject to the limits set by the bank | May have higher transaction limits |

| Cost | May have transaction fees and account fees | May have lower fees and competitive rates |

| Security | Encrypted transactions and authentication | Focus on robust security measures |

| Personalization | Personalized user experience | Customized banking solutions |

| Innovation | Embraces technological advancements | Driven by innovation and fintech solutions |

Please note that these characteristics may vary depending on the specific digital banking services or digital banks being compared.

Frequently Asked Questions

What is a digital bank?

A digital bank is a financial institution that provides banking services exclusively through digital channels, such as a website or mobile app. Digital banks do not have physical branches, which allows them to keep their costs low and pass on the savings to their customers.

What is the minimum paid-up capital for a digital bank in Bangladesh?

As per the provision of 3.1 of Guidelines to Establish Digital Bank by Bangladesh Bank, the minimum paid-up capital for a digital bank in Bangladesh is Tk. 125 crore.

What is the minimum shareholding for sponsors of a digital bank in Bangladesh?

As per the provision of 5.3 of Guidelines to Establish Digital Bank by Bangladesh Bank, the minimum shareholding for sponsors of a digital bank in Bangladesh is Tk. 50 lac.

What are the opportunities for digital banks in Bangladesh?

The opportunities for digital banks in Bangladesh are significant. The country has a large and growing population of mobile phone users, and the internet penetration rate is also increasing. This means that there is a large potential customer base for digital banks.

In addition, the Bangladesh government is supportive of the development of digital banking. The government has introduced a number of policies and regulations that are designed to make it easier for digital banks to operate in the country.

How do I open an account with a digital bank?

The process of opening an account with a digital bank is typically very quick and easy. You can usually do it online or through the mobile app. You’ll need to provide some basic information, such as your name, address, and date of birth. You may also need to provide a government-issued ID.

How do I deposit money into my digital bank account?

There are a few different ways to deposit money into your digital bank account:

- Bank transfer: You can transfer money from your existing bank account to your digital bank account.

- Cash deposit: You can deposit cash at a local agent or through the mobile app.

- Cheque deposit: You can deposit cheques through the mobile app or by mail.

How do I withdraw money from my digital bank account?

There are a few different ways to withdraw money from your digital bank account:

- Bank transfer: You can transfer money from your digital bank account to your existing bank account.

- Cash withdrawal: You can withdraw cash at a local agent or through the ATM.

- Cheque withdrawal: You can withdraw money by writing a cheque and depositing it at a bank.

How do I make payments with my digital bank account?

You can make payments with your digital bank account in a few different ways:

- Online payments: You can make online payments through the mobile app or website.

- Mobile payments: You can use your digital bank account to make payments through your mobile phone.

- In-store payments: You can use your digital bank account to make payments in stores that accept contactless payments.

How secure are digital banks?

Digital banks use the latest security technology to protect your personal and financial information. This includes things like encryption, firewalls, and fraud detection.

What are the future trends for digital banks in Bangladesh?

The future of digital banking in Bangladesh is very promising. The number of digital bank customers is expected to grow rapidly in the coming years. Digital banks are also expected to offer new and innovative products and services that will make banking more convenient and efficient.

What are the future trends for digital banks in Bangladesh?

The future trends for digital banks in Bangladesh are likely to include:

- Increased competition: More digital banks are likely to enter the market, so competition will increase.

- New product and service offerings: Digital banks are likely to offer new and innovative products and services, such as peer-to-peer lending and mobile payments.

- Stronger security measures: Digital banks will need to have stronger security measures in place to protect against cyberattacks.

- Government support: The government is likely to continue to support the development of digital banking in the country.

Last Words

The banking industry in Bangladesh has undergone significant changes over the years with the emergence of new technologies and innovations. While traditional banks continue to dominate the market, digital banks are on the way to gaining ground, offering customers a more convenient and accessible way of banking.

Leave a Reply